By Steven J. Oshins, Esq., AEP (Distinguished)

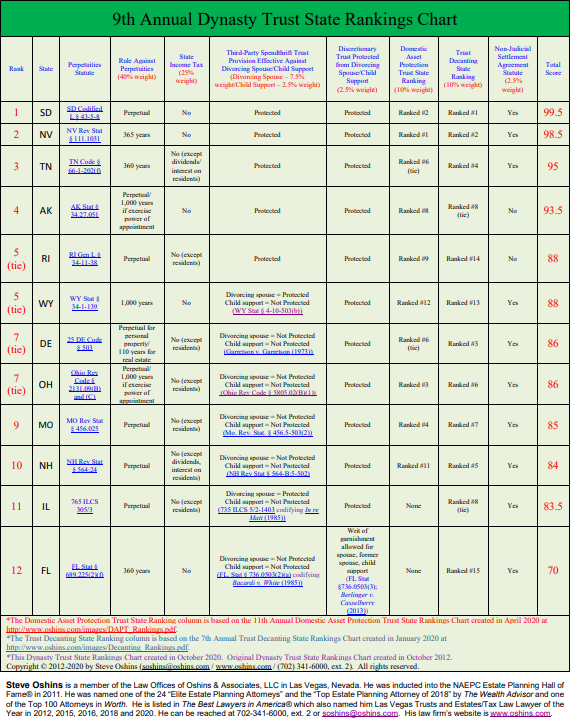

The 9th Annual Dynasty Trust State Rankings Chart has been released! This year’s Chart factors in the new era of Dynasty Trusts.

The 9th Annual Dynasty Trust State Rankings Chart has been released! This year’s Chart factors in the new era of Dynasty Trusts.

The Chart is an easy-to-use summary of leading Dynasty Trust states that shows the material differences among the states and ranks them according to usability and flexibility.

Planners often focus on the multi-generational estate tax benefits of a Dynasty Trust. However, the Tax Cuts and Jobs Act of 2017 essentially doubled the federal estate and gift tax exemption which, after inflationary increases, is now $11.58 million per person, or $23.16 million per married couple. This exemption is increasing each year by an inflationary factor, but is scheduled to be cut back in half in 2026.

Therefore, very few people are subject to a federal estate tax. This makes other Dynasty Trust benefits more valuable than the estate tax benefits for many of our clients.

DYNISTY TRUSTS

A “Dynasty Trust” is an irrevocable trust that avoids estate taxes for as long as applicable state law allows. It doesn’t necessarily have to be sitused in one of the leading Dynasty Trust jurisdictions; however, certain advantages can be obtained by doing so.

Dynasty Trusts are no longer primarily focused on estate tax savings. The Tax Cuts and Jobs Act of 2017 has changed much of the emphasis away from estate tax planning. Let’s take a look at other advantages.

CREDITOR AND DIVORCE PROTECTION

Creditor protection and divorce protection might be the most compelling reason to use Dynasty Trusts. Very simply, outright transfers are subject to the claims of the creditors and divorcing spouses of the recipients of the transferred assets.

FEDERAL AND STATE INCOME TAX SHIFTING

Income shifting is also very important. This is true both for federal income tax purposes and for state income tax purposes. A well-drafted trust will allow the trustee to sprinkle the income to taxpayers in lower tax brackets.

STATE INCOME TAX AVOIDANCE

Also, depending upon any state income tax long-arm statutes that may apply, there is often an opportunity to avoid incurring state income taxes by simply accumulating the income in a trust rather than distributing unwanted income to a beneficiary who resides in a state with a state income tax who doesn’t need or want the income.

INCOME TAX BASIS PLANNING

Passing assets in trust rather than outright allows an independent trustee or trust protector to give a beneficiary a formula general power of appointment at death over assets with an income tax basis lower than fair market value, but not over assets with an income tax basis higher than fair market value, thereby providing for basis step-ups, but not step-downs.

AVOIDANCE OF THE WIDOW’S ELECTION

If inherited assets are distributed outright to the beneficiary, then at the beneficiary’s death those assets are included in the Widow’s Election calculation for a decedent living in a common law jurisdiction, as opposed to a community property jurisdiction. For those beneficiaries who were trying to minimize their spouse’s inheritance, this can result in a very big difference in that the widow can take a percentage of these assets by electing to take against the will of the decedent.

DOWNLOAD CHART

RELATED EDUCATION

If you found this article interesting, you might also be interested in these other educational programs and products by Steve Oshins:

- Estate Planning Techniques in a Time of Low Interest Rates

- The Installment Sale to an Intentionally Defective Grantor Trust

- The Grantor Retained Annuity Trust: Significant Estate Tax Savings with Nearly Zero Gift Tax Risk

- Advanced-Level Estate Planning Sales & Marketing Kits

- Steve’s FREE State Rankings Charts

ABOUT THE AUTHOR

Steven J. Osh ins, Esq., AEP (Distinguished) is a member of the Law Offices of Oshins & Associates, LLC in Las Vegas, Nevada. He was inducted into the NAEPC Estate Planning Hall of Fame® in 2011. He was named one of the 24 “Elite Estate Planning Attorneys” and the “Top Estate Planning Attorney of 2018” by The Wealth Advisor. Steve was also named one of the Top 100 Attorneys in Worth and is listed in The Best Lawyers in America® which also named him Las Vegas Trusts and Estates Lawyer of the Year in 2012, 2015 and 2018 and Tax Law Lawyer of the Year in 2016 and 2020. He can be reached at 702-341-6000, ext. 2, at soshins@oshins.com or at his firm’s website, www.oshins.com.

ins, Esq., AEP (Distinguished) is a member of the Law Offices of Oshins & Associates, LLC in Las Vegas, Nevada. He was inducted into the NAEPC Estate Planning Hall of Fame® in 2011. He was named one of the 24 “Elite Estate Planning Attorneys” and the “Top Estate Planning Attorney of 2018” by The Wealth Advisor. Steve was also named one of the Top 100 Attorneys in Worth and is listed in The Best Lawyers in America® which also named him Las Vegas Trusts and Estates Lawyer of the Year in 2012, 2015 and 2018 and Tax Law Lawyer of the Year in 2016 and 2020. He can be reached at 702-341-6000, ext. 2, at soshins@oshins.com or at his firm’s website, www.oshins.com.