Knowing What You Don’t Know: What an Effective Financial Plan Anticipates

By Jason Oshins, Financial Advisor, MBA

Mark Twain said, “It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.” More often than not, planning is done as though the world is linear. Financial Advisors and clients make assumptions as though life moves in a straight line and nothing unexpected ever occurs. Then, when the unexpected occurs – and it will – the plan collapses.

An effective plan is dynamic, anticipating and addressing what it can, and preventing the unexpected from derailing a desired future existence. Furthermore, it builds in buffer to absorb the unexpected. This article helps clients understand what can go wrong, determine the importance of addressing these areas, and develop an action plan for mitigating them.

Oftentimes, a Financial Advisor and client will plan based on basic linear assumptions[1]. “You will get 8% every year. You’ll never get sick and need to take time off from work. Somebody else – not you or your children – will get divorced or get sued or get into an accident. Taxes will be lower once you’re in retirement. You’ll never require long term care assistance when you age. Inflation won’t prevent you from enjoying your money.” And on and on and on!

The reality? The part that “you know for sure that just ain’t so”, in Mark Twain’s words? Life happens! Both good and bad events occur, and they occur unexpectedly. Life changes its mind. And then what does it do? It changes its mind again. At times the surprises are good, at times great, at times bad, and at times downright awful. However, no matter how many surprises occur, the plan must work. Pure and simple. The alternative – a plan not working – is unacceptable. So, how do we achieve success when the pressures of life seemingly conspire against us?

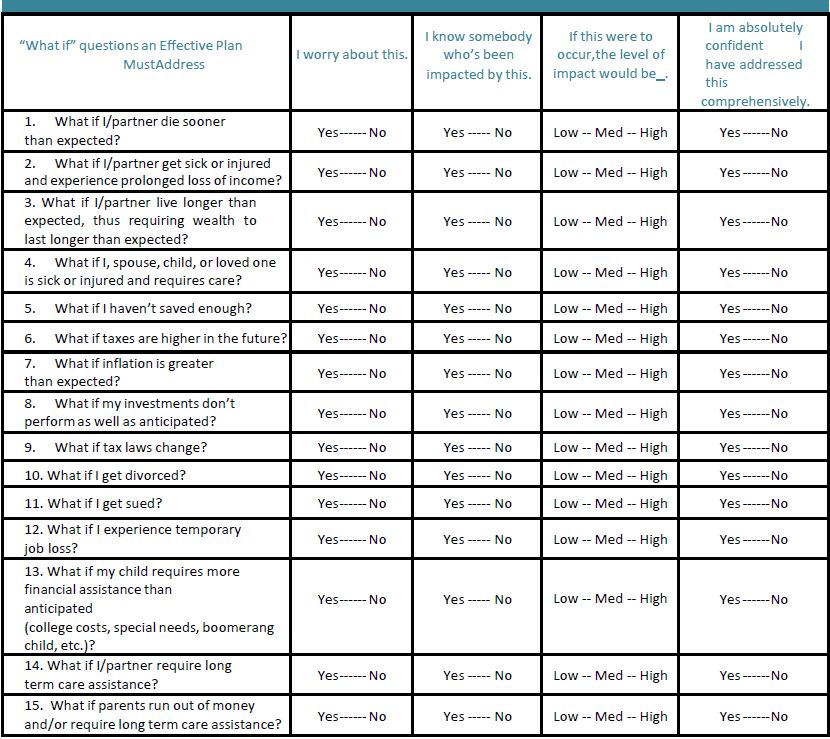

This worksheet provides a framework for assessing a plan’s preparedness. While far from comprehensive, it’s a strong starting point, serving to provoke thinking and discussion between clients and financial advisors. By answering a series of questions with honesty and confidence, the client can identify and close gaps. After all, the sooner a threat is identified, the sooner it can be addressed and marginalized. With this self-assessment, clients will gain an understanding of their level of exposure to those threats that can derail their plans. And with this understanding, they can work with their financial advisor to create a priority list, action plan, and timeline for addressing the unexpected.

Directions:

1. Answer each “what if” question for the series of statements

2. Circle all “what if” questions with (a) a high level of impact and (b) for which you don’t have absolute confidence you’ve addressed it comprehensively

3. Prioritize those you circled according to magnitude of impact to you or your family

4. Create a 60-day action plan[2] for addressing these threats

5. Repeat for those with a medium level of impact

6. Create a 180-day action plan incorporating these additional threats

An effective plan – one that works no matter what – anticipates and provides for the unexpected. It provides buffer to absorb the unexpected. It’s dynamic. It’s not based on linear assumptions that can’t possibly come true. Mark Twain also said, “Don’t go around saying the world owes you a living. The world owes you nothing. It was here first.” Life happens. An effective plan knows this and anticipates this. An effective plan works.

CITATIONS:

[1] This list could have a seemingly infinite number of items. Included are several additional examples. Have they saved sufficiently? Will retirement last longer than they anticipate, thus requiring their wealth to last longer? Will their parents outlive their wealth? Will their parents need long term care assistance? Will their children require additional assistance? Will their children’s college last longer than four years? Will inflation be greater than anticipated? Etc.

[2] A simple action plan template for an advisor and client to use includes rows of “what if” items listed in priority order, along with columns of (1) action to take, (2) beginning date, and (3) completion date. Ultimately, whatever commits the client to action to address the “what ifs” is effective. Once clients understand the critical nature of addressing a specific threat, the role of the advisor is to prevent procrastination.

ABOUT THE AUTHOR

Jason Oshins is a Wealth Management Advisor and Certified Exit Planner with WestPac Wealth Partners. He works closely with clients throughout the country to increase wealth during lifetime, improve income during retirement, and provide a greater legacy upon passing, while also protecting their estates from taxes, inflation, and market volatility. He specializes in the areas of estate planning, investments, retirement planning, insurance planning and design, disability protection, long-term care, wealth transfer, and business planning. Jason obtained his MBA from the University of Michigan in Ann Arbor. He can be reached at (702) 470-2753 or by e-mail at [email protected]

This material contains the current opinions of the author but not necessarily those of Guardian or its subsidiaries and such opinions are subject to change without notice. Guardian, its subsidiaries, agents, and employees do not provide tax, legal, or accounting advice. Consult your tax, legal, or accounting professional regarding your individual situation.

Registered Representative and Financial Advisor of Park Avenue Securities LLC (PAS). OSJ: 5280 Carroll Canyon Rd. Suite 300 San Diego, CA 92121 619.684.6400. Securities products and advisory services offered through PAS, member FINRA, SIPC. Financial Representative of The Guardian Life Insurance Company of America® (Guardian), New York, NY. PAS is a wholly owned subsidiary of Guardian. WestPac Wealth Partners, LLC is not an affiliate or subsidiary of PAS or Guardian. Insurance products offered through WestPac Wealth Partners and Insurance Services, LLC, a DBA of WestPac Wealth Partners, LLC. CA Insurance License # 0G03153 | 2023-160980 Exp. 09/25

OTHER ARTICLES IN THIS ISSUE

- PRACTICE-BUILDING: “Multiple Financial Advisor Referral Relationships May Be a Big MISTAKE!” by Philip J. Kavesh, J.D., LL.M. (Taxation), CFP®, ChFC, California State Bar Certified Specialist in Estate Planning, Trust & Probate Law

- SUPPORT & ADMINISTRATIVE STAFF: “Top 10 E-mail Etiquette Rules for Estate Planning Professionals (and Their Assistants and Staff)” by Kristina Schneider, Executive Assistant

- ESTATE TAX PLANNING: “Feeling the Burn: The Importance of the Tax Burn in Estate Tax Planning” by Steven J. Oshins Esq., AEP (Distinguished)

- TAX PLANNING: “Reducing Or Eliminating Capital Gains On The Sale Of Businesses And Real Estate” by Bruce Givner, Esq.