By Steven J. Oshins Esq., AEP (Distinguished)

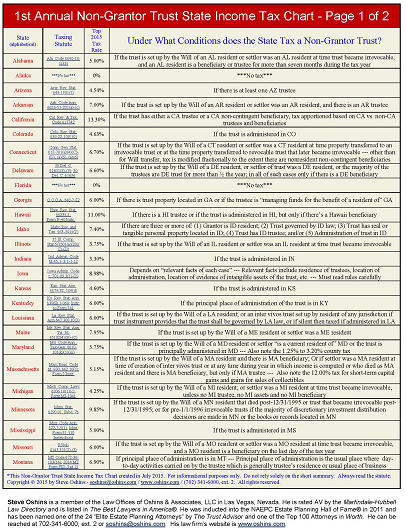

The 1st Annual Non-Grantor Trust State Income Tax Chart is a two-page summary of the non-grantor trust state income tax rules in all states and Washington, D.C. The Chart can be accessed by clicking here.

The 1st Annual Non-Grantor Trust State Income Tax Chart is a two-page summary of the non-grantor trust state income tax rules in all states and Washington, D.C. The Chart can be accessed by clicking here.

Each state and Washington, D.C. is listed in alphabetical order with the applicable statutory cite that is linked to the online taxing statute. Each jurisdiction’s taxing rules are described briefly so the user can generally know the rules without having to read through the entire statute.

The online user should always click the link to the applicable statute to understand any details. The Chart also lists the highest tax rate so the end user can appreciate the value of saving that tax for the client’s trust.

State Taxation of a Non-Grantor Trust

There must be thousands of existing non-grantor trusts that are needlessly paying state income tax on income that isn’t distributed.

Different states have different rules as to what creates a “resident trust” that is subject to taxation in that state. Depending upon the state statute, a state may tax a trust based on one or more of the following reasons:

- A testamentary trust set up in the Will of the resident testator

- An inter vivos trust set up by a resident of that state

- A trust that is being administered in that state

- A trust with a resident trustee

- A trust where there is a beneficiary who is a resident of that state

Avoiding the Tax by Fixing the Trust

The opportunity to avoid a state income tax on the undistributed income of a non-grantor trust often makes a substantial impact on the value of the trust’s underlying assets. By avoiding the tax drag inherent in a trust that is subject to state income tax, the trust grows in value much faster.

Depending upon the state rules, sometimes this is as simple as having a resident trustee resign or simply moving the administration of the trust to a different jurisdiction.

Other times, it will take more creativity, such as by decanting the trust or moving the situs of a trust to a trust situs that allows decanting to then decant the trust to modify it in such a way that it will avoid state income tax. [Decanting is a technique permitted by statute in 22 states that allows the trustee to distribute the assets from one irrevocable trust into a new irrevocable trust with different terms for one or more beneficiaries of the first trust.]

Modifying the ongoing state income tax might be next-to-impossible if the state taxes a trust solely based on the residency of the testator or settlor. This might require a court challenge to the constitutionality of the taxing statute.

Conclusion

This new chart, called the 1st Annual Non-Grantor Trust State Income Tax Chart, should open up opportunities for practitioners to save state income tax for their clients by moving and fixing any existing trusts that are needlessly paying state income tax.

ABOUT THE AUTHOR

Steven J. Osh ins, Esq., AEP (Distinguished) is an attorney at the Law Offices of Oshins & Associates, LLC in Las Vegas, Nevada, with clients throughout the United States. He is listed in The Best Lawyers in America®. He was inducted into the NAEPC Estate Planning Hall of Fame® in 2011 and was named one of the 24 Elite Estate Planning Attorneys in America by the Trust Advisor. He has authored many of the most valuable estate planning and asset protection laws that have been enacted in Nevada. He can be reached at 702-341-6000, ext. 2, at soshins@oshins.com or at his firm’s website, www.oshins.com.

ins, Esq., AEP (Distinguished) is an attorney at the Law Offices of Oshins & Associates, LLC in Las Vegas, Nevada, with clients throughout the United States. He is listed in The Best Lawyers in America®. He was inducted into the NAEPC Estate Planning Hall of Fame® in 2011 and was named one of the 24 Elite Estate Planning Attorneys in America by the Trust Advisor. He has authored many of the most valuable estate planning and asset protection laws that have been enacted in Nevada. He can be reached at 702-341-6000, ext. 2, at soshins@oshins.com or at his firm’s website, www.oshins.com.

OTHER ARTICLES IN THIS ISSUE

- PRACTICE BUILDING: “The GREAT Debate of 2015: The Client Maintenance Plan vs. The Free Service Package” by Philip J. Kavesh, J.D., LL.M. (Taxation), CFP®, ChFC, California State Bar Certified Specialist in Estate Planning, Trust & Probate Law

- SUPPORT & ADMINISTRATIVE STAFF: “Squash the Drama: 5 Steps to Properly Handling Interoffice Conflicts” by Kristina Schneider, Executive Assistant

- FINANCIAL PLANNING: “Planning for the Three Phases of Life” by Jason Oshins, Financial Advisor, MBA

- TAX PLANNING: “Federal Income Tax Planning for Trusts” by Robert S. Keebler, CPA/PFS, MST, AEP (Distinguished), CGMA

- FINANCIAL PLANNING” “Financial Advisor: Attract Generation X & Y Clients” by Mark Dreschler, President & CEO at Premier Trust and Deborah Erdmann, QKA, CISP, Vice President & Trust Officer at Premier Trust