Skip to content

About

How We Help

About Philip Kavesh

Why Choose Us

FAQ

Education

Instant Download Programs

Practice Management

Marketing

About the Speakers

E-Books

White Papers

Blog

California Specialist Exam Prep Course

Event

Event FAQs

Products

Legal Document Forms

Instant Download Programs

Coaching

Media & Publications

Marketing Tools

Attorneys

Practice Management & Marketing

Seminar Marketing

Coaching

Free Strategy Session

Free Resources

CPAs

Educational Programs

Robert Keebler Monthly Bulletin

Robert Keebler Charts

White Papers

Financial Advisors

Sell More Life Insurance

Educational Programs

E-Books

White Papers

Contact

Book a Free Strategy Session

About

How We Help

About Philip Kavesh

Why Choose Us

FAQ

Education

Instant Download Programs

Practice Management

Marketing

About the Speakers

E-Books

White Papers

Blog

California Specialist Exam Prep Course

Event

Event FAQs

Products

Legal Document Forms

Instant Download Programs

Coaching

Media & Publications

Marketing Tools

Attorneys

Practice Management & Marketing

Seminar Marketing

Coaching

Free Strategy Session

Free Resources

CPAs

Educational Programs

Robert Keebler Monthly Bulletin

Robert Keebler Charts

White Papers

Financial Advisors

Sell More Life Insurance

Educational Programs

E-Books

White Papers

Contact

Book a Free Strategy Session

1.866.754.6477

Search

Login

Cart

1.866.754.6477

Search

Search

About

How We Help

About Philip Kavesh

Why Choose Us

FAQ

Education

Instant Download Programs

Practice Management

Marketing

About the Speakers

E-Books

White Papers

Blog

California Specialist Exam Prep Course

Event

Event FAQs

Products

Legal Document Forms

Instant Download Programs

Coaching

Media & Publications

Marketing Tools

Attorneys

Practice Management & Marketing

Seminar Marketing

Coaching

Free Strategy Session

Free Resources

CPAs

Educational Programs

Robert Keebler Monthly Bulletin

Robert Keebler Charts

White Papers

Financial Advisors

Sell More Life Insurance

Educational Programs

E-Books

White Papers

Contact

Book a Free Strategy Session

Home

»

Advanced Planning

»

Page 5

Browse by Category

Advanced Planning

Asset Protection

Uncategorized

Announcement

Niche Areas of Planning

Same-Sex Estate Planning

Estate Planning

Elder Law

IRA Trusts

Court Cases

Promotions

Financial Planning

Free Resources

Coaching

IRA & Retirement Benefit Planning

Life Insurance Planning

Marketing

Referral Relationships

Seminars

Digital & Internet Marketing

Practice-Building

Support & Administrative Staff

Systems & Processes

Mindset & Self-Care

Best Practices

Tax Planning

Estate Tax Planning

Gift Tax Planning

Income Tax Planning

Search

Search

Advanced Planning

Showing 41–50 of 86 results

Default sorting

Sort by popularity

Sort by average rating

Sort by latest

Sort by price: low to high

Sort by price: high to low

The Spousal Lifetime Access Trust

See Details

The Philosophy Behind Protecting Assets from Creditors

See Details

Which Trust Jurisdiction is a “Champ-Champ”?

See Details

Steve Oshins: Interview About the 2019 State Rankings Charts and State Income Tax Chart

See Details

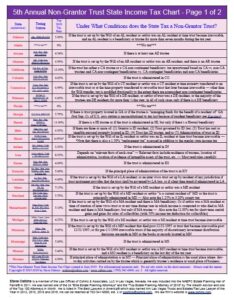

The Kaestner Case and the New Emphasis on Using Non-Grantor Trusts to Save State Income Tax

See Details

Using a Corporate Trustee to Obtain Jurisdiction in a First-Tier Trust State

See Details

The Strange Case of Dr. Jekyll and Mr. Oshins: DAPTs vs. Hybrid DAPTs

See Details

The Strange Case of Dr. Jekyll and Mr. Oshins: Nevada vs. Delaware Dynasty Trusts

See Details

What Trust Jurisdictions Other than Alaska, Delaware, Nevada and South Dakota Are Best?

See Details

Grantor Retained Annuity Trusts for the Large Estate

See Details

« Previous

1

…

3

4

5

6

7

…

9

Next »

Contact Us

First Name *

Last Name

Phone

Email *

Area of Expertise

Please select one

CPA

Estate Planning Attorney

Financial Advisor

Life Insurance Agent

Other

Message *

Enter the above code:

Send Us Your Message