By: Robert S. Keebler, CPA/PFS, MST, AEP (Distinguished), CGMA

An important provision within the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 (“2010 Tax Relief Act”) allows an executor of an estate of a married decedent the option to transfer any unused estate tax exemption amount to the surviving spouse.[1] Thus, for example, if a decedent used only a portion of his or her estate tax exemption, the estate could elect to have the remaining portion pass to the surviving spouse, giving the surviving spouse a larger estate tax exemption.[2] Although this portability provision seems simple on the surface, it introduces important planning considerations and traps for the unwary.

Portability: An Overview

When Congress created portability it gave us several new terms. The Basic Exclusion Amount (BEA) is the minimum estate tax exclusion amount allowed for a single decedent. The BEA is set by statute and indexed for inflation. Congress set it at $5,000,000 for 2011 and inflation increased the exemption to $5,120,000, $5,250,000, and $5,340,000 for those who died in 2012, 2013, and 2014 respectively. However, the BEA is reduced by prior taxable gifts.

The Deceased Spousal Unused Exclusion Amount (DSUE) is the estate tax exclusion amount a deceased spouse may transfer to the surviving spouse. It equals the deceased’s unused BEA. DSUE cannot exceed the lessor of: (1) the statutory BEA or (2) the BEA of the last deceased spouse minus the amount on which the tentative tax on the estate of the last deceased spouse is determined. DSUE is calculated when the first spouse dies and is not indexed for inflation.[3]

Most importantly, note that the election to transfer the unused exemption amount must be made on a timely filed estate tax return (Form 706).[4] This means that many individuals will need to file an otherwise unnecessary return merely to make the election. Many practitioners are missing this key step, thereby creating significant issues for their clients. As of January 1, 2015 the only way to correct a missed election is by obtaining 9100 relief.

Furthermore, by making the election, the statute of limitations remains open for the decedent spouse’s estate tax return until the statute of limitations has run on the surviving spouse’s estate tax return.[5] Thus, the IRS can audit the deceased spouse’s estate tax return (even after the normal statute of limitations has run) and add any increase in tax to the surviving spouse’s estate tax return.

Deceased Spousal Unused Exclusion Amount

The transfer of DSUE is limited by a number of rules. First, only the DSUE from the last deceased spouse may transfer to the surviving spouse; a surviving spouse cannot aggregate DSUEs or choose the largest DSUE from previously deceased spouses. Secondly, transfer of DSUE requires marriage or privity.

Example 1. Last deceased spouse. H1 and W1 are married at the time of H1’s death in 2011. Although H1’s taxable estate is $5,000,000, the executor of H1’s estate transfers the entire estate to W1 (via the unlimited marital deduction) and elects to transfer H1’s entire estate tax exclusion amount ($5,000,000) to W1 (i.e., DSUE). W1 then marries H2. In 2012, H2 dies with a taxable estate of $3,000,000, and the executor of H2’s estate chooses to utilize $3,000,000 of H2’s $5,120,000 estate tax exclusion amount. Based on these facts, the DSUE available to W1 is $2,120,000 (i.e., H2’s remaining estate tax exclusion amount).

Example 2. Privity. H1 and W1 are married at the time of H1’s death in 2011. The executor of H1’s estate transfers the entire estate to W1 (via the unlimited marital deduction) and elects to transfer H1’s entire estate tax exclusion amount ($5,000,000) to W1 (i.e., DSUE). W1 then marries H2. In 2012, W1 dies with a taxable estate of $3,000,000, and the executor of W1’s estate chooses to utilize $3,000,000 of W1’s $5,120,000 estate tax exclusion amount. Based on these facts, the DSUE available to H2 is $2,120,000 (i.e., W1’s remaining estate tax exclusion amount).

- While W1 had a $10,120,000 total estate tax exclusion amount ($5,000,000 DSUE from H1 + $5,120,000 BEA), only $3,000,000 was used.

- Of the $3,000,000 estate tax exclusion that was used, the entire amount was attributable to W1’s BEA.

- Therefore, only $2,120,000 of W1’s total estate tax exclusion amount (i.e. $5,120,000 BEA – $3,000,000 BEA used) may be utilized by H2.

- It is important to note that W1’s $5,000,000 DSUE estate tax exclusion amount from H1 is completely lost and cannot be used by H2.

Analysis of the Portability Election

The mechanics of how the exclusion transfers between individuals is not terribly complicated. However, analyzing whether to make the portability election can be. There are a number of factors which affect this decision:

- Size of combined estate;

- Anticipated growth of the surviving spouse’s estate;

- Changes in the future estate tax law;

- Asset protection issues; and

- Additional basis step-up of property in surviving spouse’s taxable estate.

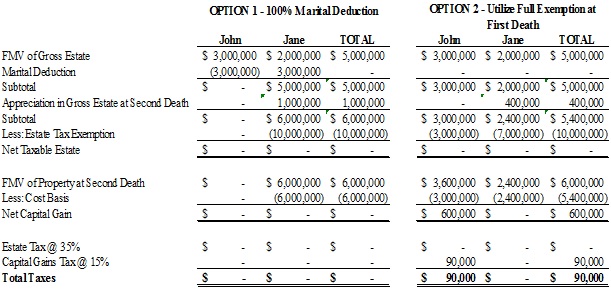

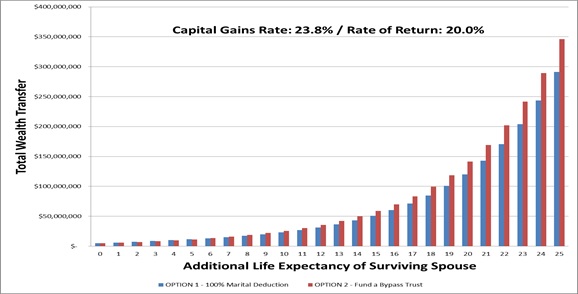

Example 3. John and Jane have a combined estate of $5,000,000. Assume that John dies in 2011 and Jane dies later that year when the value of her total estate is $6,000,000.

The couple had two options at John’s death. The first was to transfer property to Jane using the Marital Deduction, making the exemption unneeded. The second option would be to use a portion of John’s exemption.

The couple incurs some capital gains tax by utilizing the exemption at John’s death and since their combined estate is below the combined exclusion amount, taking John’s exemption at his death increases their tax liability. However, as the following chart illustrates, if Jane significantly outlives John, choosing to utilize the full exemption at John’s death may be prudent.

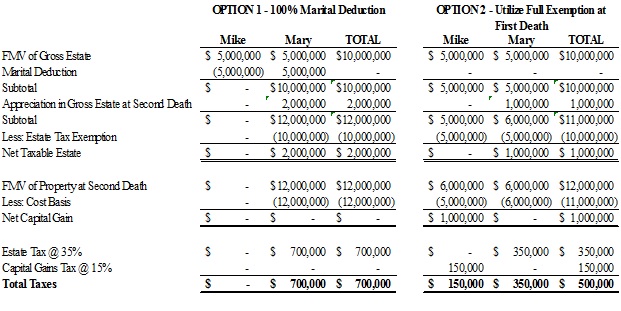

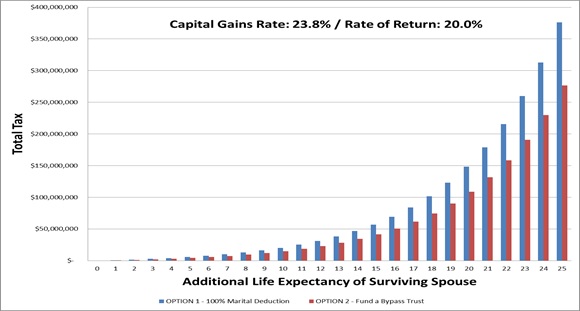

Example 4. Mike and Mary have a combined estate of $10,000,000. Assume that Mike dies in 2011 and that at Mary’s death at the end of 2011 the value of the total estate is $12,000,000.

The couple incurs some capital gains tax by utilizing the exemption at Mike’s death, however since their combined estate is above the combined exclusion amount because of its growth after Mike’s death, taking Mike’s exemption at his death decreases their tax liability.

Note that the couple does save some tax by utilizing the full exemption amount at the first death; however, the potential savings increase the longer the surviving spouse lives. In this case, given the huge assumed growth rate, the resulting tax savings are dramatic.

In addition to the effect explained in Examples 3 & 4, moderate wealth taxpayers should have other considerations which might include:

- State estate tax in decoupled states will remain a substantial cost;

- Inflation may push their estates above the thresholds; and

- The future may bring a lower exclusion amount; “Wait and see” may turn into “Wait and pay”

- Asset protection and related concerns.

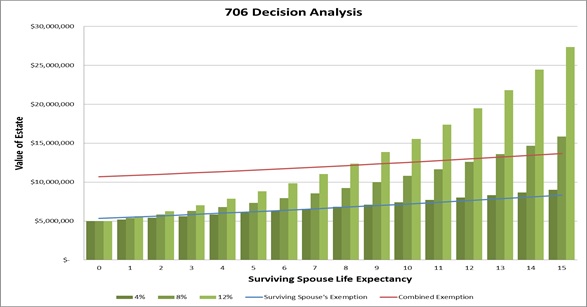

Example 5. Assume that an estate planning practitioner encounters a couple with a gross estate of $5M. The couple is resistant to filing Form 706 because of the associated costs. Depending on their circumstances, that resistance to incur the associated costs might be prudent or very short sighted as the following chart demonstrates:

The above chart projects the resulting size of the estate in relation to the two possible exemption amounts and considering three possible growth rates. Clearly, the higher the growth rate and the longer the surviving spouse lives, the more planning that is necessary. Once an estate’s value exceeds the surviving spouse’s BEA (the blue line), it is prudent to file a Form 706 for portability. Once an estate value exceeds the combined value of the DSUE and BEA (the red line), it is prudent to consider a bypass trust.

Conclusion

Understanding portability and using it strategically can have a significant impact on taxpayers. The initial steps to understanding the new scheme and remembering to file for the election are overwhelmingly simple and important. The advanced strategy, that is analyzing whether to utilize the exemption at the first death or to wait until the second death, is considerably more complicated, has a narrow application, and involves more unknowns; however, it is very powerful.

CITATIONS:

[1] The American Taxpayer Relief Act of 2012 made the portability of estate tax exemption permanent.

[2] It should be noted that portability does NOT allow the decedent’s unused portion of the GST tax exemption to transfer to the surviving spouse.

[3] Section 303 of the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010; IRS Form 706; Reg. § 20.2010-2T(b)(1).

[4] No election can be made on a late-filed return.

[5] However, the “adequate disclosure” rules (applying to post-1997 gifts) do NOT apply.

RELATED PRODUCTS & EDUCATION

Join us and Bob Keebler on Thursday, May 7, 2015 at 9am Pacific Time (12pm Eastern Time) for a 90-minute teleconference entitled, “Mathematics of Portability”. For more information and to register, click here.

ALSO, when you register for this teleconference, you have the option to also purchase Robert Keebler’s Portability CalculatorTM.

This portability analysis needs to be done BEFORE you even file the election. How can you do this analysis as scientifically as possible, and do it quickly (even with the client right in front of you)?

This portability analysis needs to be done BEFORE you even file the election. How can you do this analysis as scientifically as possible, and do it quickly (even with the client right in front of you)?

There’s an answer.

Nationally renowned tax and estate planning expert, Robert S. Keebler, CPA, MST, AEP (Distinguished), CGMA, has put together a brand new tool known as…The Portability CalculatorTM.

With this special and timely calculator, you can simply and easily weave the portability discussion into any client or prospect meeting – – in just 15 minutes or less – – and generate significant additional revenue (or referrals to other professionals that will come back to you in kind).

Bob Keebler’s Portability CalculatorTM includes everything you need so you can, step-by-step, conduct effective portability conversations. >>MORE INFO

ABOUT THE AUTHOR

Robert S. Keebler CPA/PFS, MST, AEP (Distinguished), CGMA is a partner with Keebler & Associates, LLP and is a 2007 recipient of the prestigious Accredited Estate Planners (Distinguished) award from the National Association of Estate Planning Counsels and has been named by CPA Magazine as one of the Top 100 Most Influential Practitioners in the United States. Mr. Keebler is the past Editor-in-Chief of CCH’s magazine, Journal of Retirement Planning, and a member of CCH’s Financial and Estate Planning Advisory Board. Mr. Keebler frequently represents clients before the National Office of the Internal Revenue Service (IRS) in the private letter ruling process and has received over 150 favorable private letter rulings. Mr. Keebler is nationally recognized as an expert in family wealth transfer and preservation planning, charitable giving, retirement distribution planning and estate administration and works collaboratively with other professionals on academic reviews and papers, as well as client matters. He can be reached at (920)593-1701 or at robert.keebler@keeblerandassociates.com.

OTHER ARTICLES IN THIS ISSUE

- PRACTICE-BUILDING: “The Top 10 Seminar Planning & Marketing Mistakes Attorneys Make!” by Philip J. Kavesh, J.D., LL.M. (Taxation), CFP®, ChFC, California State Bar Certified Specialist in Estate Planning, Trust & Probate Law

- SUPPORT & ADMINISTRATIVE STAFF: “Helpful Computer Programs for Organization and Efficiency” by Megan DeLaGarza, Executive Assistant

- ASSET PROTECTION: “New Single Member LLC Veil Piercing Case Is a Wakeup Call to Attorneys and Spells Opportunity” by Mason D. Salisbury, J.D.