By Robert S. Keebler, CPA, MST, AEP (Distinguished), CGMA

By Robert S. Keebler, CPA, MST, AEP (Distinguished), CGMA

Earlier this year, the IRS released PLR 201417027 in which it refused to extend the deadline to begin required minimum distributions (RMDs), for taxpayers who were not even aware that they were beneficiaries of a decedent’s retirement plan. Because of their seemingly innocent mistake, the missed RMDs might be sliced in half by the 50% excise tax for missed distributions under IRC § 4947(a) and the beneficiaries might be exposed to negligence and understatement penalties under IRC § 6662. This ruling is a reminder of the importance of proper naming of beneficiaries to IRAs and other retirement plans.

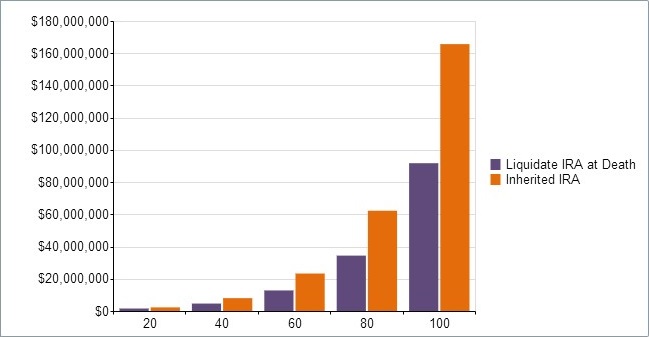

Value of an Inherited IRA

Careful naming of IRA beneficiaries is critical. The PLR makes it clear that merely putting a name on the beneficiary form is insufficient; a certain amount of thought, communication, and coordination is required to prevent loss of family wealth to taxation.

Moreover, an IRA owner who wishes to pass on as much wealth as possible would be well-advised to carefully consider who should be named as a beneficiary. This is because wealth grows more quickly in the tax-free or tax-deferred environment inside an IRA. Beneficiaries who do not need the IRA funds for support should name the youngest possible designated beneficiaries to spread distributions over the longest possible time period. This minimizes RMDs, leaves more money to grow inside the IRA at its pre-tax rate of return and maximizes the amounts that can be passed on to heirs.

The following chart shows the long term value of properly naming a young beneficiary, a grandchild for example, compared to liquidating a $1,000,000 IRA at the account owner’s death.1

The chart clearly depicts the compounded value the tax-preferred treatment of an inherited IRA over several generations. It is an obvious must to do the proper planning which usually means the youngest acceptable person is named the beneficiary of the IRA or the IRA is rolled over to the surviving spouse who names a very young beneficiary.

A Trust as an IRA Beneficiary

However, naming an individual as beneficiary may lead to serious problems. Such problems may include:

- The IRA owner has no control over how the assets will be managed or distributed after his or her death;

- The IRA owner cannot protect the assets from creditors after his or her death;

- The IRA owner has no control over who receives the IRA payments after the death of the primary beneficiary;

- The IRA owner has no control over how fast payments are made; and

- The IRA owner has less certainty that RMDs will be made as required.

Naming a trust as beneficiary can solve all of these problems. Careful planning is necessary, however, to create the best possible result for the family and to avoid traps for the unwary.

There is a special rule under Reg. § 1.401(a)(9)-4, Q&A 5 that permits an IRA owner to name a trust as beneficiary of his or her IRA and have the oldest trust beneficiary (and not the trust itself) treated as the designated beneficiary for RMD purposes if four requirements are satisfied:

- The trust is valid under state law, or would be but for the fact that there is no corpus;

- The trust is irrevocable or will by its terms become irrevocable upon the death of the IRA owner;

- The beneficiaries of the trust can be identified from the trust instrument; and

- Proper documentation has been provided to the plan administrator.

If the trust does not meet all four requirements, the IRA will be treated as having no designated beneficiary.

It is almost always advisable to create a stand-alone trust specifically designed to be an IRA beneficiary rather than using an existing trust created for another purpose, such as a living trust. The goals of the IRA beneficiary trust and the living trust may be inconsistent and trying to combine them often leads to unintended results.

Example. Suppose that Taxpayer wishes to benefit a number of contingent beneficiaries in his or her living trust, but including these beneficiaries will shorten the stretch-out period for paying out the IRA. By trying to combine the two trusts, the client might lose either estate planning flexibility or tax deferral. To accomplish both objectives, separate trusts may be needed.

For more information about The IRA Inheritance Trust® Legal Document Form & Technical Training Package, click here.

Spousal Rollover Option

The Internal Revenue Code provides a very favorable option when the surviving spouse is the sole beneficiary of an IRA. The spouse can roll the IRA over into his or her own IRA and name new beneficiaries (e.g., his or her children), greatly increasing the deferral period (IRC §402(c)(9)). As an added benefit, if the IRA owner dies before the surviving spouse reaches his or her required beginning date, the IRA owner can delay the start of distributions until reaching age 70 ½ (Reg. § 1.401(a)(9)-3(a)(3)(B)). Also, if it is a Roth IRA the spouse will not be required to take any distributions either.

The IRS has taken the position, however, that this option is only available if the surviving spouse has total control over the disposition of the plan assets (PLR 200944059). Thus, the spouse must ordinarily be the outright beneficiary of the IRA pursuant to a specific beneficiary designation (Reg. § 1.408-8, Q&A 5(a)). If anyone other than the surviving spouse controls the IRA proceeds (e.g., a trustee other than the surviving spouse), a rollover is generally not available (PLR 9851050). Giving the surviving spouse a power to withdraw the trust assets would make it possible to do a spousal rollover (PLRs 200950053 and 200928045), as would making the spouse the trustee of the credit shelter trust with the power to control distributions (See, for example, PLRs 200943046 & 200831025).2 If the spousal rollover is not available, the life expectancy of the surviving spouse would have to be used instead of the life expectancy of the oldest child and distributions to the surviving spouse would begin when the IRA owner died.

Correcting Unfavorable Beneficiary Designations

Ideally, the IRA owner will plan ahead and have a favorable designated beneficiary when he or she dies. Mistakes are often made in naming beneficiaries, however, shortening the deferral period.

Fortunately, beneficiary designations can be improved with post-mortem planning. Because only individuals or entities who are beneficiaries both when the IRA owner dies and on September 30 of the year following the IRA owner’s death are countable for purposes of determining a designated beneficiary, there is a window period for correcting unfavorable beneficiary designations. This window period, which could last from just over nine months to just under 21 months, can be used to eliminate unwanted beneficiaries that shorten the payout period.

Beneficiaries can disclaim an interest in an IRA if: (1) they meet all the general requirements for a qualified disclaimer under IRC § 2518; and (2) the disclaimer is made by September 30 of the year following the IRA owner’s death. The general requirements for a qualified disclaimer are as follows:

- There must be an irrevocable and unqualified refusal by a person to accept an interest in property;

- The refusal must be in writing;

- The written refusal must be given to the transferor of the interest within nine months after the date on which the transfer creating the interest is made;

- The disclaiming person hasn’t accepted the interest or any of its benefits; and

- As a result of such refusal, the interest passes without any direction on the part of the person making the disclaimer and passes either (a) to the spouse of the decedent, or (b) to a person other than the person making the disclaimer (IRC § 2518(b)).

Note that as a practical matter, the September 30 deadline does not really change the general requirements. The nine-month period can never end after September 30 of the year following the IRA owner’s death and, in most cases, will expire long before that date.

Disclaimers are generally used to eliminate an older individual as a countable beneficiary. This makes a younger person with a longer life expectancy the designated beneficiary; thus decreasing the required minimum distributions.

A second option is to cash out a beneficiary’s interest before September 30 of the year following death. This is done by simply paying the beneficiary to be eliminated such beneficiary’s interest in the IRA. This method might be used to eliminate non-individuals like charities that have no life expectancy and might be unwilling to disclaim.

Conclusion

Careful naming of IRA beneficiaries is critical to prevent undue wealth loss to taxation. It is important that it is coordinated with the remainder of estate plan and non-mathematical considerations made to determine if utilizing a trust is appropriate. Careful planning is of tremendous value with regard to the inheritance of IRAs.

CITATIONS:

[1] Assumptions: 25 year old beneficiary, $1,000,000 IRA balance at death, a pre-tax growth rate of 7%, and both account owner & beneficiary’s tax rate is 30%.

[2] Giving the spouse control over the trust assets would cause the assets to be included in his or her estate under IRC §2042, eliminating the benefit of the credit shelter trust.

RELATED EDUCATION & PRODUCTS

Below is a list of a number of educational programs and products that relate to this topic that you might be interested in:

- The IRA Inheritance Trust® Legal Document Form & Technical Training Package

- Traditional IRA Distribution Flowchart

- Roth IRA Distribution Flowchart

- Explaining the Top Ten IRA Mistakes to Clients and Their Beneficiaries with Michael J. Jones, CPA

- Special Tax Planning for Large IRAs

- How to Market & Sell More IRA Beneficiary Trusts

- The Tools & Techniques of Employee Benefit & Retirement Planning, 13th Edition – By Stephan R. Leimberg and John J. McFadden

ABOUT THE AUTHOR

Robert S. Keebler, CPA, MST, AEP (Distinguished), CGMA is a partner with Keebler & Associates, LLP and is a 2007 recipient of the prestigious Accredited Estate Planners (Distinguished) award from the National Association of Estate Planning Counsels. He has been named by CPA Magazine as one of the Top 100 Most Influential Practitioners in the United States and one of the Top 40 Tax Advisors to Know During a Recession. Mr. Keebler is the past Editor-in-Chief of CCH’s magazine, Journal of Retirement Planning, and a member of CCH’s Financial and Estate Planning Advisory Board. His practice includes family wealth transfer and preservation planning, charitable giving, retirement distribution planning, and estate administration. Mr. Keebler frequently represents clients before the National Office of the Internal Revenue Service (IRS) in the private letter ruling process and in estate, gift and income tax examinations and appeals.

In the past 20 years, he has received over 150 favorable private letter rulings including several key rulings of “first impression.” Mr. Keebler is nationally recognized as an expert in estate and retirement planning and works collaboratively with other experts on academic reviews and papers, and client matters. Mr. Keebler is the author of over 75 articles and columns and editor, author, or co-author of many books and treatises on wealth transfer and taxation, including the Warren, Gorham & Lamont of RIA treatise Esperti, Peterson and Keebler/Irrevocable Trusts: Analysis with Forms.

He is a frequent speaker for legal, accounting, insurance and financial planning groups throughout the United States at seminars and conferences on advanced IRA distribution strategies, estate planning and trust administration topics including the AICPA’s Advanced Estate Planning, Personal Financial Planning Conference and Tax Strategies for the High Income Individual Conference.

To contact Mr. Keebler, call his office at 920-593-1701 or by e-mail at robert. keebler@keeblerandassociates.com.

OTHER ARTICLES IN THIS ISSUE

- MARKETING: “I Had a Successful Practice, Now What?” by Joseph J. Strazzeri, J.D.

- LIFE INSURANCE: “Top Five Life Insurance Myths” by Steven J. Oshins, J.D., AEP (Distinguished)

- MARKETING: “The Top 20 Seminar Marketing Mistakes People Make (Part 2 of 2)” by Philip J. Kavesh, J.D., LL.M. (Taxation), CFP®, ChFC, California State Bar Certified Specialist in Estate Planning, Trust & Probate Law

- LIFE SETTLEMENTS: “What’s the Truth About Life Settlements” by Daxton Fryer, Senior Life Settlements Analyst

Image courtesy of photostock / FreeDigitalPhotos.net